What makes predictive analytics work? Good data, great algorithms, smart statisticians? Yeah sure, that stuff helps but none of it makes predictive analytics work. In my experience the most critical thing in making analytics work is a an operational business leader with the experience and vision to see them integrated into their business. I know this sounds like the old adage about CRM solutions not being about the software but being about the people and processes. In fact it is, and maybe doubly so for predictive analytics and decision management because the whole goal of an analytics solution is the tell operations (marketing, sales, customer service, collections, etc...) the right decision and get them to do the right thing.

Last week I got a call from a client. This experienced operational manager, Scott C., understands what makes analytics work and how to apply them to make his operations work better. Instead of waiting for his analytics group to suggest uses for predictive analytics Scott keeps a constant eye out for decisions that he and his team make that could be improved (made more profitably, faster and more consistently) through predictive scores and decision rules.

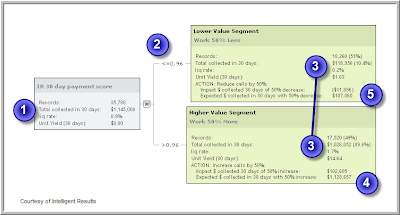

Scott's called last week was about a situation with his current collections and recovery group. Like the settlement offer pricing and outsourcing decisions we've helped him with in the past, Scott is looking for an application that will tell his managers which accounts are right for a specialized treatment they've developed. The catch of course is that this treatment, while effective, is expensive. Our goal is to develop predictive models and strategies that optimize this new treatment's use given the bank's goals and constraints.

In this way Scott is leveraging analytics, not to replace operations but to supercharge it. Scott knows that only his operational team could have come up with the new treatment but that only analytics can prescribe it's use for optimal impact. When analytics are embraced by operations in this way new solutions are quickly developed for decisions that the analytics side of the business may never have known existed. What's more, because these new solutions are directly aligned with the operation's goals (bonuses) they are often better understood and more quickly adopted.